Traders have good causes to love Walmart (NYSE: WMT). Initially, it is the largest retailer on this planet with practically $650 billion in trailing-12-month income. Its greater than 10,600 shops carry every part from groceries to dwelling items to auto elements and extra.

Briefly, buyers can at all times count on customers will patronize Walmart — it sells nearly every part and its large shops are conveniently positioned to serve communities all through the nation. In different phrases, it is not a enterprise that buyers want to fret about.

Here is one other optimistic: Walmart’s e-commerce operations are actually a $100 billion annual enterprise. And having a digital platform of this scale permits the corporate to develop its promoting enterprise, which might be an vital driver for earnings within the coming years.

That stated, it is doable to criticize Walmart inventory from an funding perspective proper now. When trying on the inventory’s valuation from a number of views, this is among the least well timed moments to purchase it up to now decade.

Walmart’s price-to-sales (P/S) ratio is at a 10-year excessive. Its price-to-earnings (P/E) ratio is greater than the common for the S&P 500. And the corporate’s dividend yield is at a 10-year low.

Due to this fact, I wish to spotlight three different low cost retail chains I like greater than Walmart as funding alternatives proper now: Ollie’s Discount Outlet Holdings (NASDAQ: OLLI), 5 Under (NASDAQ: FIVE), and Greenback Normal (NYSE: DG).

1. Ollie’s Discount Outlet

Earnings progress tends to drive rising inventory costs, and that is excellent news for shareholders of Ollie’s. The pandemic hit the corporate’s profitability, creating provide chain points and added labor bills. However Ollie’s bounced again in 2023 with an enormous 74% enhance in working revenue, and future progress appears possible.

In 2024, Ollie’s plans to open 48 new places, which is good progress from the 512 places it had on the finish of 2023. And buyers can count on new openings at a speedy clip for a while, contemplating administration simply elevated its long-term aim to 1,300 shops.

Revenue margins for Ollie’s have traditionally held regular because it has grown. It is a good motive to consider that administration has a deal with on the enterprise and may preserve profitability sturdy because it expands. Due to this fact, with lots of of recent shops within the pipeline, I count on earnings to extend for Ollie’s, resulting in upside for the inventory value.

2. 5 Under

The funding thesis for 5 Under is just like that of Ollie’s: The corporate has worthwhile shops and plans to open many extra, resulting in earnings progress and upside for buyers. The distinction between these two, nevertheless, is that 5 Under has a extra outlined (and aggressive) timeline.

There have been greater than 1,500 5 Under places on the finish of 2023. However administration intends to have greater than 2,600 places by the tip of 2026 and greater than 3,500 places by the tip of 2030.

Understand that 5 Under is totally debt-free as a result of its price to open a brand new retailer is comparatively low and the payback interval is only one yr. Consider it like a cash-flow snowball rolling downhill. The corporate is worthwhile, and makes use of money to open new places. These places rapidly pay for themselves, and the cash-flow snowball grows.

The excellent news for buyers proper now could be that 5 Under inventory is down about 16% yr so far, giving buyers a greater entry level for a long-term funding.

3. Greenback Normal

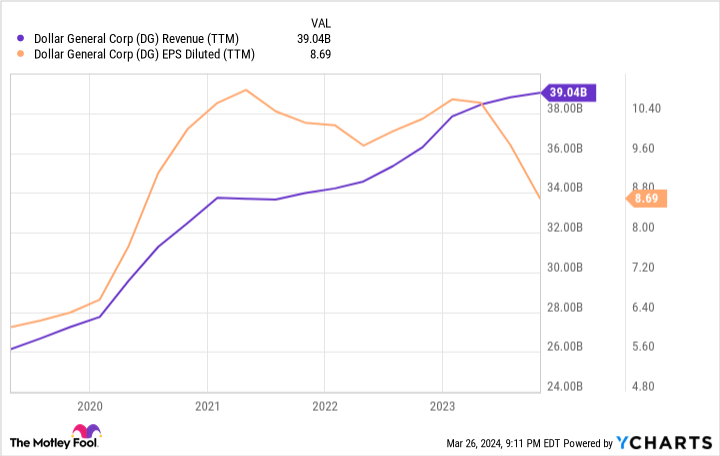

Whereas enterprise is buzzing for Walmart, Ollie’s, and 5 Under, Greenback Normal has some issues. On one hand, its income is at an all-time excessive, powered each by new places and same-store gross sales progress at present shops. Nevertheless, its diluted earnings per share (EPS) fell in 2023, and so they’re anticipated to fall once more in 2024.

The silver lining is that Greenback Normal remains to be seeing loads of shopper demand, and it’s nonetheless worthwhile. Due to this fact, this enterprise is salvageable. Administration simply must determine the issues which can be protecting its earnings down and repair them.

In actuality, Greenback Normal already is aware of that the important thing drawback is sub-optimal stock administration, and it is working to appropriate it. Based mostly on administration’s steerage, the turnaround will not be full this yr. However I consider it can occur prior to later, boosting the corporate’s earnings by a shocking quantity within the coming years.

Within the meantime, those that purchase Greenback Normal inventory at the moment will be rewarded whereas they wait. Not like Ollie’s or 5 Under, Greenback Normal inventory pays a dividend. The yield is greater than Walmart’s — one more reason to want Greenback Normal. And on prime of that, Greenback Normal inventory will possible enhance its payout once more in 2024, simply because it has carried out for eight straight years.

In abstract, I perceive why buyers love Walmart inventory, however it’s not essentially a superb worth proper now. Due to this fact, for buyers who love the low cost retail area, Ollie’s, 5 Under, and Greenback Normal supply higher alternatives for earnings progress. I would purchase shares of all three at the moment earlier than shopping for shares of Walmart.

Must you make investments $1,000 in 5 Under proper now?

Before you purchase inventory in 5 Under, think about this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they consider are the 10 greatest shares for buyers to purchase now… and 5 Under wasn’t certainly one of them. The ten shares that made the reduce may produce monster returns within the coming years.

Inventory Advisor supplies buyers with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of March 25, 2024

Jon Quast has positions in Greenback Normal and 5 Under. The Motley Idiot has positions in and recommends Walmart. The Motley Idiot recommends 5 Under and Ollie’s Discount Outlet. The Motley Idiot has a disclosure coverage.

3 Low cost Retail Shares That I would Purchase As we speak Earlier than Shopping for Walmart Inventory was initially printed by The Motley Idiot